It is November already, and it’s thus time to look back at the financials of October 2021.

I was happy to see my investments were (overall) back in green this month. Consecutive red months are always bad for moral, but we know from history that Q4 are typically “rebound time” for the global markets. Indeed it seems that the dip we saw in August-September has now been wiped out completely, so it seems history repeats itself once again 🙂

Unfortunately external circumstances means that I’ve had to put Total Balance contributions on pause for a little while. Surging energy prices (among other things) meant that our budget came up short in October, so I had to add some extra cash to our budget (buffer for the coming months) and also something else happened!

I got a new job. Again…

The month in review

Yes, I got a new job again! Well, I’ve held my current job for more than 3 years now, so I suppose it was time 😉

I’ve been working in the financial sector where they pay you in advance (so you actually get money before you’ve started working 😛 ). I’m now leaving the financial sector in favor of the green energy sector, which pay you backwards. – Meaning you don’t get paid until after you’ve worked there for a month. I’m not gonna lie, I prefer being paid in advance 😛

But what this means is that I won’t be getting any salary the 1st of December. So I’ve had to pause any contributions to my Total Balance for a couple of months to cover my living costs in December/January. It will even itself out eventually, and the double-salary that I received 3 years ago when I left the green energy sector (yes, I’m going back!) is of course now embedded in my Total Balance, so I could simply just pull it out again. – But I don’t want to sell any of my assets right now! 😉

Anyway, this new job will give me a slight monthly increase in monthly net income, but unfortunately it will see a big decrease in pension contributions (it’s a young company so they don’t have any pension contributions as part of the package). They do have an employer provided pension scheme though, but the company is not paying anything towards it – but the employee has a mandatory contribution of at least 8% of your salary. Not ideal, but I might actually decide to pay more than that (tax optimizing). This is the price that I have to pay to work for a young(er) company with a green profile. Hopefully they will eventually decide to give their employees a raise in form of a pension contribution, but for now these are the terms that I’ve accepted (much to my wife’s annoyance, as I’ve also have to forfeit 2 weeks of paid vacation – I have 7 weeks vacation in my current job)…

I’m hoping that these “sacrifices” (let’s get real here, it’s still a nice deal, all things considered) will ultimately give me a higher sense of job satisfaction, as I’ve been unhappy in my current job for a long time. My new job will require more hands-on work (Cloud stuff), and I’m hoping that my small contribution to “saving the planet” is going to mean that my daughter (and her future kids) will still be able to live on it for the remainder of their lives…

Anyway, October was a great month for my Crypto assets, so I’m glad that I made a small move in that direction 🙂

Our Pensions have now also recovered nicely from the market dip in September. While patience is not my strong suit, I am getting better and better at handling these market corrections. I’ve seen plenty of them by now, so while I try not to follow the market on a day-to-day basis, news of RED days typically always finds a way to reach me. When they do I make sure to NOT log in to my brokerage account. “Stay calm and carry on” is the mantra (most of the time!…) 🙂

And in other news: we finally got a new house appraisal from the bank. It was (as expected) very good news. While Covid-19 has been terrible to our health (in general), it has not been bad for home equity in- and around the major cities. Our house is now worth 20% more (conservatively estimated) than what we paid for it 4 years ago (we live in the capital region).

When inflation is running rampant, buckle up and double-down on (cheap) debt…This is what we intend to do, and since our LTV is now < 60% we’re eligible to get a 30-Year interest-only loan. Yes, 30 years without paying down your principal. Outrageous! This would have never been a good idea in previous generations, but with the interest rate being < 2%, my money will work better for me in the market than in my bricks.

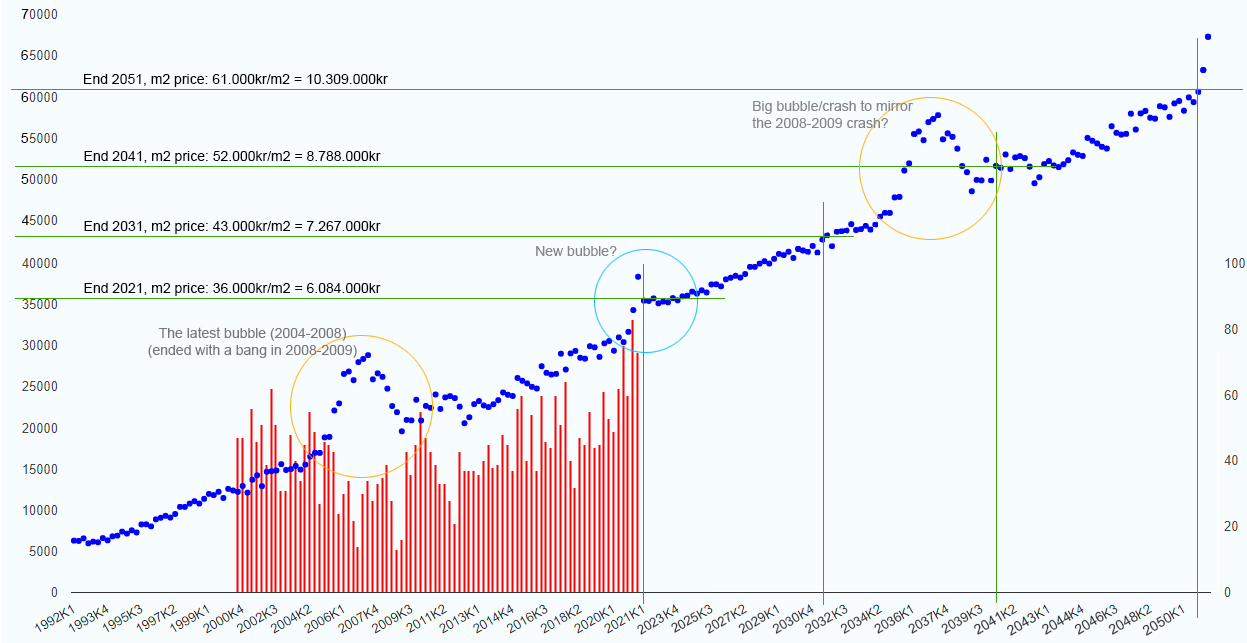

Last month I made a projection of how much our house could be worth, provided that the next 30 years will play out similar to the previous 30.

I can’t get enough of this graph (I’m a graph-nut!), so lets just repeat it here! This was how it looked:

IF the current trend continues (ignoring what appear to be a new bubble growing) our LTV will drop to 48% in 2031 – even without paying down our principal. In 2041 we’ll be at 40% (perhaps?).

It will certainly be interesting to follow the progress in the coming years. Either way, our plan is now to transfer our principal payments to our Total Balance (investments) instead. This will hopefully come in effect at the beginning of 2022 (currently negotiating the details with the bank).

The pretty graphs

Our Net Worth (Page-3) has taken a big leap this month due to our new home appraisal. For a long time my Pension and our Equity has been in a neck-to-neck race, but the equity has now left my pension in the dust (again). Hopefully it will catch up again eventually 😉

My wife’s pension has also been doing well in October, so it’s pretty much on par with our Total Balance. So the plan for 2022 is to divert more funds towards our Total Balance (instead of adding more equity), so hopefully it’ll be an interesting race to follow! 😀

The boring income statement

| Platform | Invested | Transactions | Last month | Current value | Monthly income |

| Commodities | |||||

| GOLD (Coins) | € 5,333 | € 0 | € 5,500 | € 5,500 | |

| € 5,500 | € 5,500 | ||||

| Stocks (Dividend portfolio) | |||||

| Bank of Nova Scotia (BNS) | € 1,000 | € 0 | € 1,293 | € 1,345 | € 0 |

| PROREIT (PRV.UN) | € 2,018 | € 0 | € 4,045 | € 4,047 | € 17 |

| Shaw Communications (SJR) | € 2,000 | € 0 | € 3,252 | € 3,143 | € 7 |

| Toronto Dominion Bank | € 1,000 | € 0 | € 968 | € 1,012 | € 0 |

| TransAlta Renewables (RNW) | € 2,000 | € 0 | € 2,503 | € 2,441 | € 8 |

| € 12,061 | € 11,988 | € 32 | |||

| Stocks (Indices) | |||||

| iShares Global Clean Energy (IQQH) | € 6,667 | € 7,168 | € 7,526 | € 0 | |

| iShares MSCI World Min Volatility (IQQ0) | € 6,667 | € 7,357 | € 6,996 | € 0 | |

| € 13,930 | € 14,522 | € 0 | |||

| Properties | |||||

| The-Many (Brickshare) | € 15,999 | € 0 | € 16,034 | € 16,034 | € 0 |

| Property #1 | € 68,667 | € 0 | € 68,667 | € 68,667 | € 0 |

| Fundbricks | € 1,333 | € 0 | € 1,333 | € 1,333 | € 0 |

| € 86,034 | € 86,034 | € 0 | |||

| Crypto | |||||

| ADA | € 40 | € 43 | |||

| BTC | € 78 | € 91 | |||

| DOT | € 50 | € 67 | |||

| ETH | € 777 | € 988 | |||

| € 945 | € 1,189 | € 5 | |||

| Cash | |||||

| Bank #1 cash (main savings) | € 0 | -€ 267 | -€ 267 | ||

| Bank #2 Opportunity money | € 0 | € 0 | € 0 | ||

| Broker account (CAD, EUR, DKK) | € 32 | € 356 | € 388 | ||

| € 89 | € 121 | ||||

| Total balance | € 118,559 | € 119,354 |

My small Crypto portfolio (with Celsius.network) generated a small passive income of €5 in October. Not a lot! But hopefully it will continue to grow over time 🙂

My dividend stocks produced the standard amount of dividends, so this month was fairly ordinary. I hope to eventually be able to add more dividend-paying assets, but given the current cash flow drought it’s unlikely that it will happen anytime soon, unfortunately! Oh well, patience is a virtue… 😉

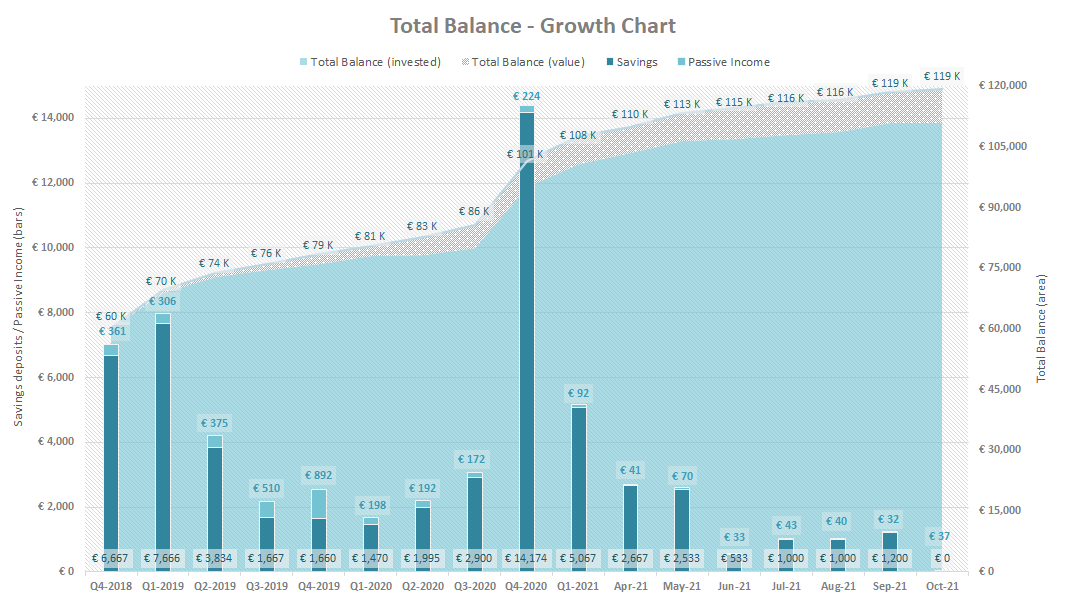

The classic growth chart

As always I include the Classic Growth Chart for tracking purpose.

I know! Those zero-savings months looks terrible in this format. AAAAAARGGH my graphics heart is bleeding. Oh well 🙂

Unfortunately, next month will also be a zero-savings month 🙁

In Conclusion (TL;DR)

All in all it was an average passive income month, and our stock portfolios (including our pensions) have now surged to new highs once again.

I’ve got a new job again (will start in December) and this will have a short-term negative impact on my savings. Hopefully it will pick up again come the new year 😉

We got hour house appraised and as a result we’ve now got almost €300.000 worth of equity in our house. Pretty crazy. So we’ve decided to stop paying down on the mortgage principal and instead divert the funds towards our Total Balance, which means that it will be invested instead of being stored in our bricks. This will (hopefully) come into full effect at the beginning of 2022 where we plan to remortgage.

That’s it for this month, folks!

Hope to see you again next month, and thanks for reading this far! 😉

Congratulations the job, Nick! It sounds like it could turn out to also be more motivational regarding doing something more “meaningful”.

Anyways, fellow Dane here that just stumpled upon your blog now. I look forward to dig deeper into how you construct your style of FIRE, and hopefully I can learn alot from you. 🙂

Hi Alexerander, thanks for stopping by, and good luck with your håndværker tilbud! It looks like you’re almost there 😉

I’m curious: how do you guys invest your savings? 🙂

Haha, thank you! It might look that way, but there are still a few years of work left (basement, garden, garages, etc.) 😀 The joke goes: “Vi mangler bare lige det sidste…”

Kinda boring to be honest: We have some crypto, which we are staking to get some yield on it, and our monthly investment goes into a yield paying stock index (Sparindex DJSI World). We do some stockpicking stuff in the company I run, so I really just wanted our personal savings to be as simple as possible. At the moment a big portion of our savings is going into the house (and coming baby), but in a few years I really want to start looking for a holiday home (sommerhus), that we can rebuild and then sell or rent out.

And thanks alot for your feedback on the posts!

Congrats on your new job Nick, higher sensation of a meaningful life in exchange of less attractive bonus packages is a wise decision.

Nice jump on net worth, man you’ll be a millionaire sooner than me, I’ll stop sticking around here if that happens 😉

Thanks! I sure hope its worth it to switch now. But my pension seem to be doing great on its own these days, so I figured it’ll be ok without any major contributions for a while 😛

It turns out the best investments I’ve made so far are the houses I’ve lived in. We made a decent profit when we sold our first home, and now our second home is already up more than 20%. It’s crazy. Especially since that growth is tax free. That’s hard to beat…

We were at a dinner party with parents from my kids school the other night, and they were also talking about the prices going completely bananas in their area (close to her school is kinda posh). Some had bought their house back in the 2004/2005 and it has almost tripled in value!

Our main concern with those valuations are now that the taxes is going to follow! (Home/land tax has been capped for years by a previous government. I doubt that the current government is going to let it continue though)..

If I compare it with my area the price went down over the last 10 years and you must pay taxes after selling. Obviously, other locations as BCN o Madrid have done well, but the tax bit is still not helpful. Becoming richer is more of a challenge in Spain.

Anyway, well done and may the upper trend go with you 🙂